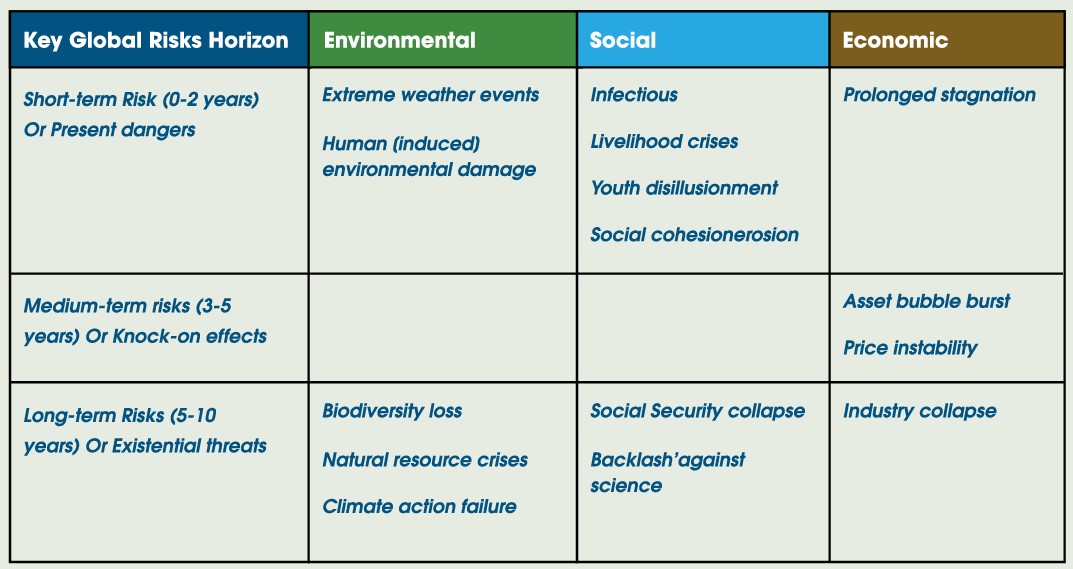

Table-1 Global Risk Exposure

Over the years, there has been growing stakeholder pressure on the top management of companies to look beyond financial performance alone.

Organizations must excel in all three dimensions of sustainability performance (environmental, social, and economic). Against the backdrop of the above-mentioned global risk factors and as economies are emerging from the shock of COVID-19- 19, the chorus is growing loud to embrace the sustainable development model and integrate sustainability perspectives within organizational strategic policy.

Adopting Sustainability is increasingly seen as a responsible business practice and a fiduciary duty of business leaders. Most importantly. Operating within the holistic sustainability criteria is a prudent business decision to reduce negative socio-ecological impacts and mitigate risk exposure.

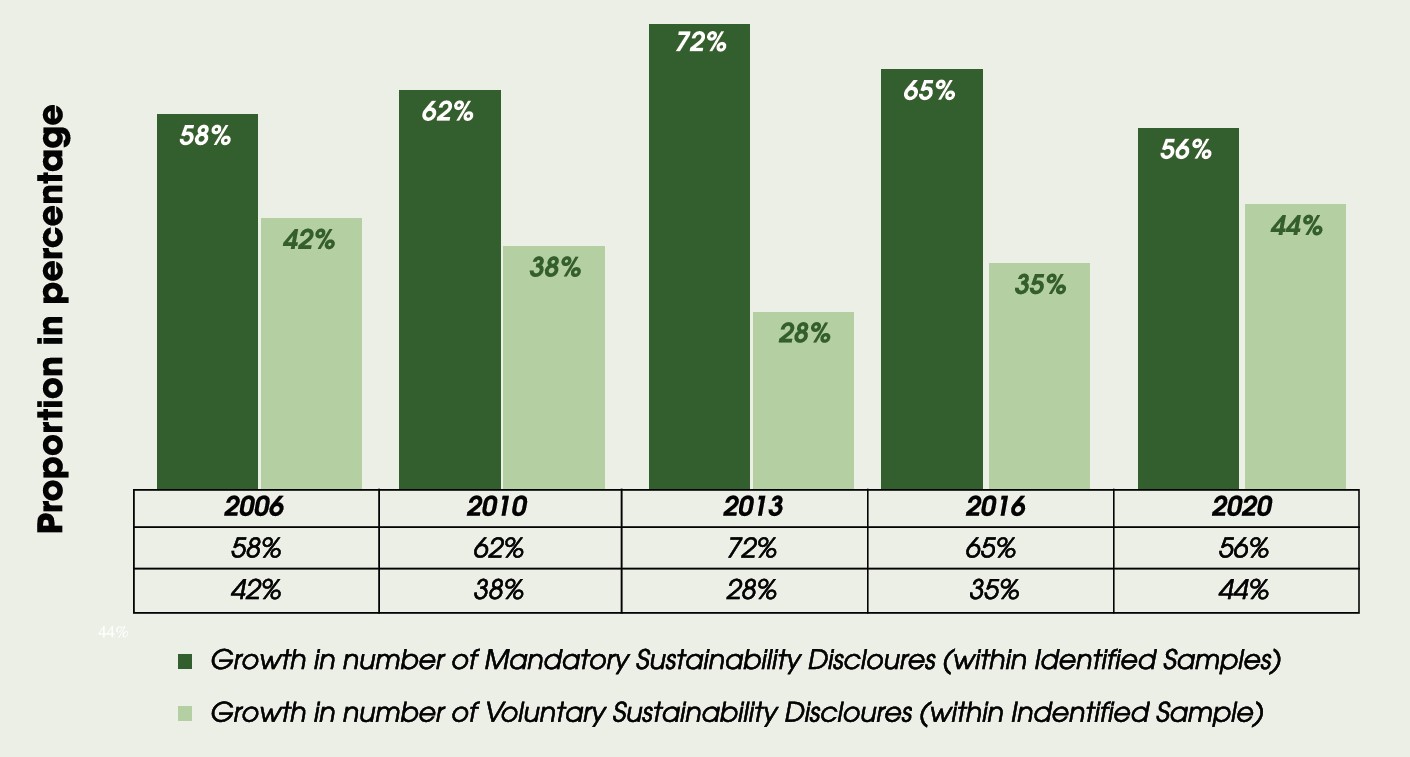

Sustainability practices: from a Voluntary to a Mandatory regime

After prolonged intellectual debate and activism by various stakeholders, Sustainability is an influential policy agenda within the statutory and regulatory frameworks.

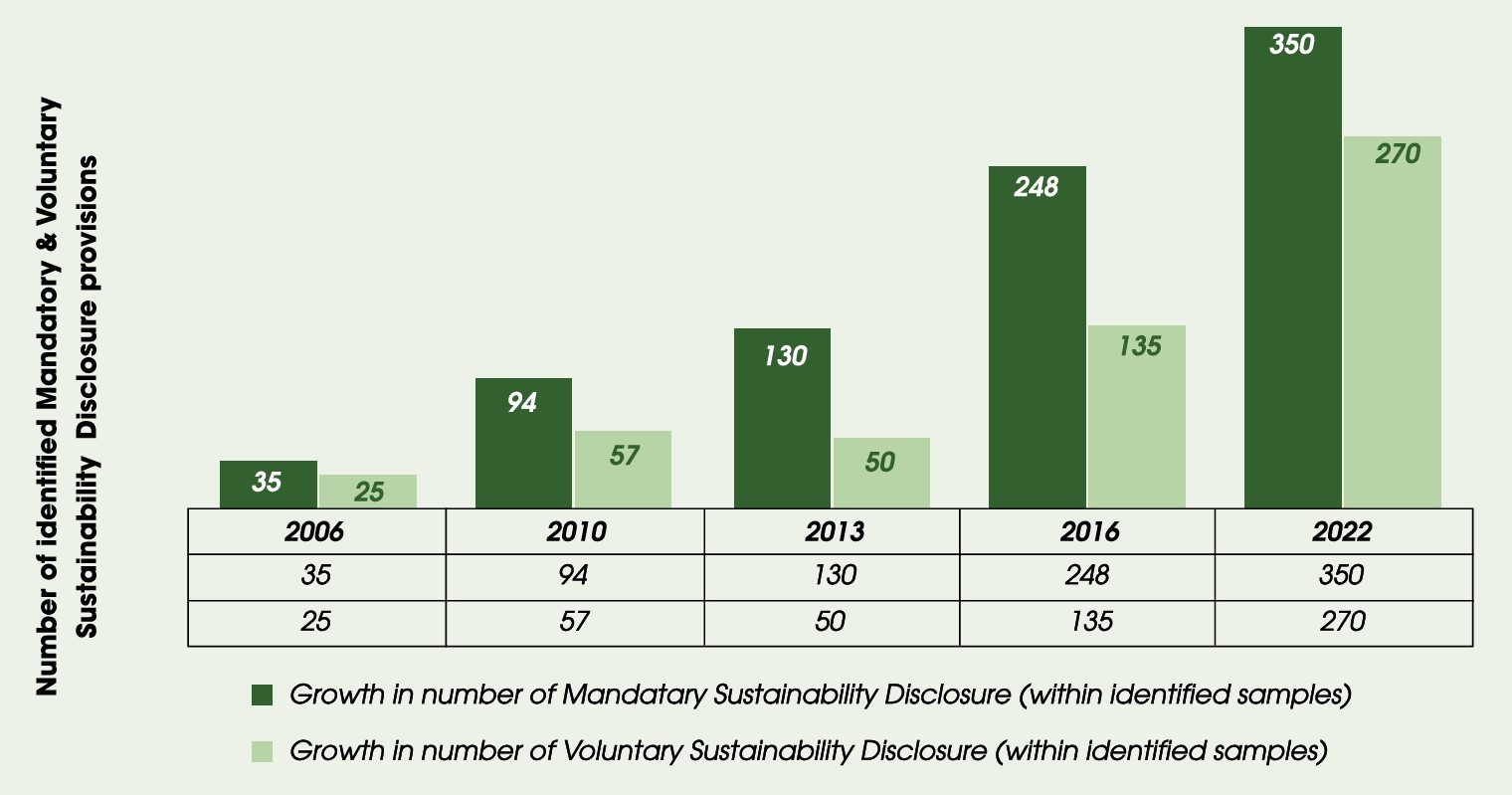

Today, Sustainability is no longer a voluntary disclosure obligation in many jurisdictions as organizations are mandated to disclose the positive or negative impacts of their operation’s environmental, social, and economic impacts. In addition, stakeholders, including investors, are interested in knowing about an organization’s risk exposure from a holistic sustainability perspective.

About 45 countries across the globe have enacted about 140 laws and regulatory standards that mandate companies to disclose some aspect of a company’s sustainability performance. For example, the Czech Republic updated its accounting law in 2017 and prescribed that all large entities with more than 500 employees must report on their non-financial performance. In 2017, France transposed its ‘1180 Ordonnance’ based on the European NFRD into French law. In 2019, the Securities and Exchange Board of India (SEBI) instructed its top 1000 companies to publish Business Responsibility Reporting (BRR).

In 2017, Germany adopted the European NFRD and instructed all listed financial and non-financial companies with more than 500 employees to report on certain sustainability information. In 2018, Japan adopted TCFD recommendations and revised its Environmental Reporting Guidelines.

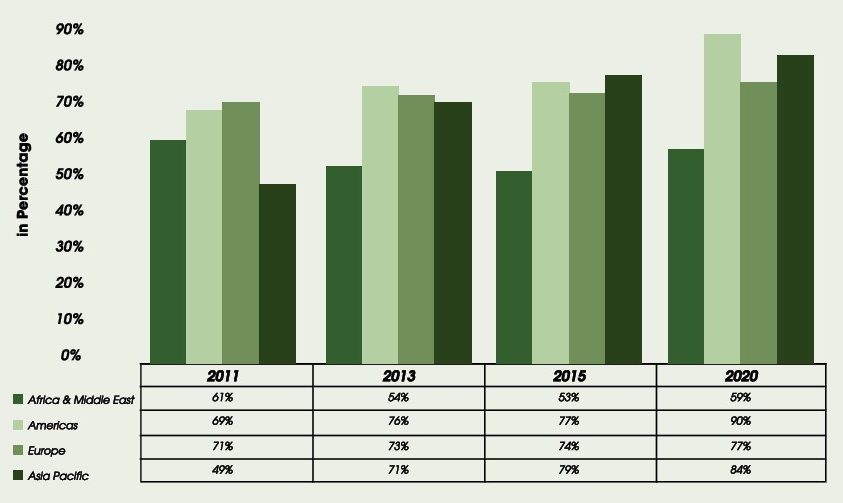

In 2018, Nigeria’s Securities and Exchange Commission (SEC) approved the Nigerian Stock Exchange’s Sustainability Disclosure guidelines. In 2018, Pakistan adopted the Sustainable Development Goals in its National Framework. In 2019, the UK introduced the Net Zero 2050 commitment in law and instructed UK’s listed companies to publish information based on TCFD recommendations from 2022. The Abu Dhabi Stock Exchange (ADX) has formally committed to incorporating sustainability aspects in the financial market in partnership with the United Nations-led initiative: The Sustainable Stock Exchange Initiative (SSE).

In addition, 15 stock exchanges have prescribed formal guidelines on sustainability reporting to their listed companies.

Contemporary Sustainability or ESG Frameworks

Many voluntary non-financial reporting frameworks and standards have evolved with a growing regulatory shift towards non-financial disclosures.

The five most prominent contemporary sustainability reporting or ESG frameworks and standards have been promulgated by:

∅ The Global Reporting Initiatives (GRI),

∅ International Integrated Reporting Council (IIRC) or Integrated Reporting (IR),

∅ Sustainability Accounting Standard Board (SASB),

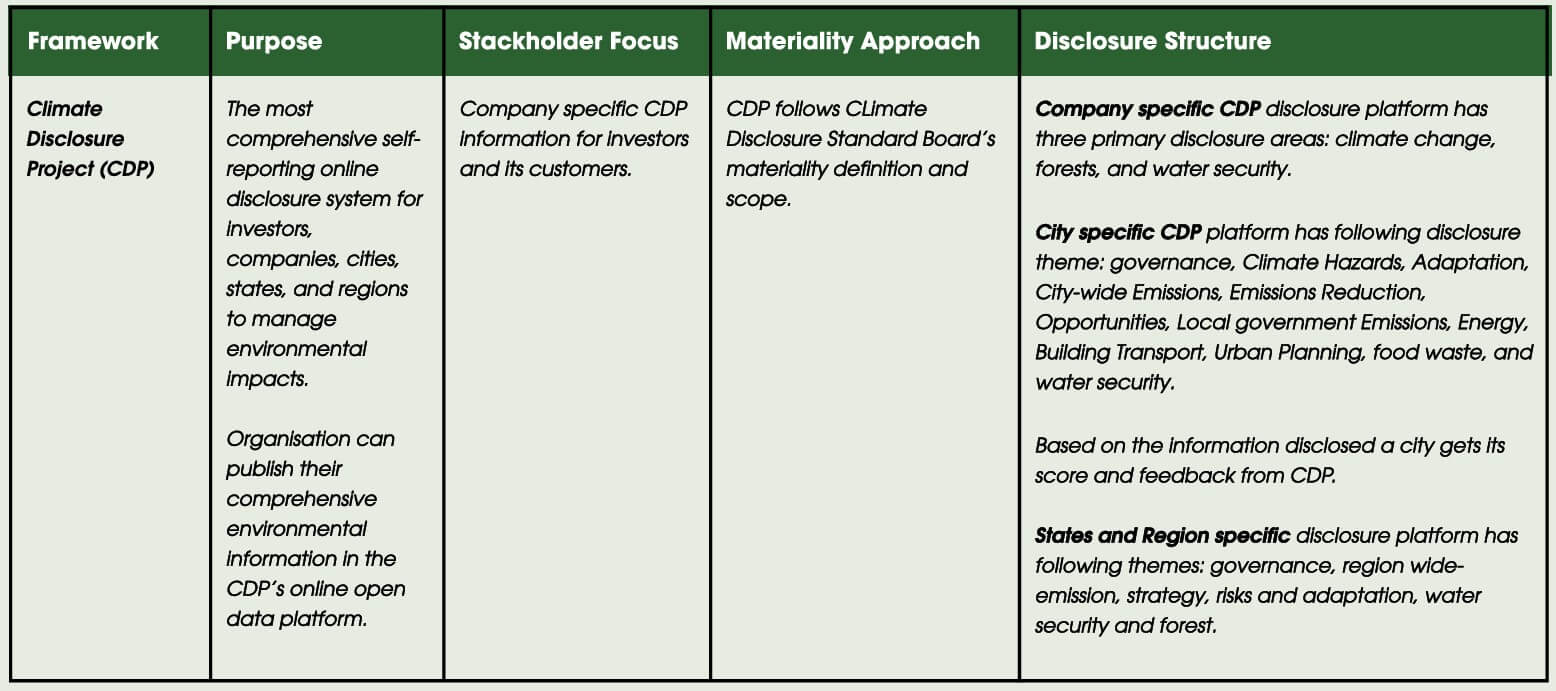

∅ Climate Disclosure Project (CDP) and

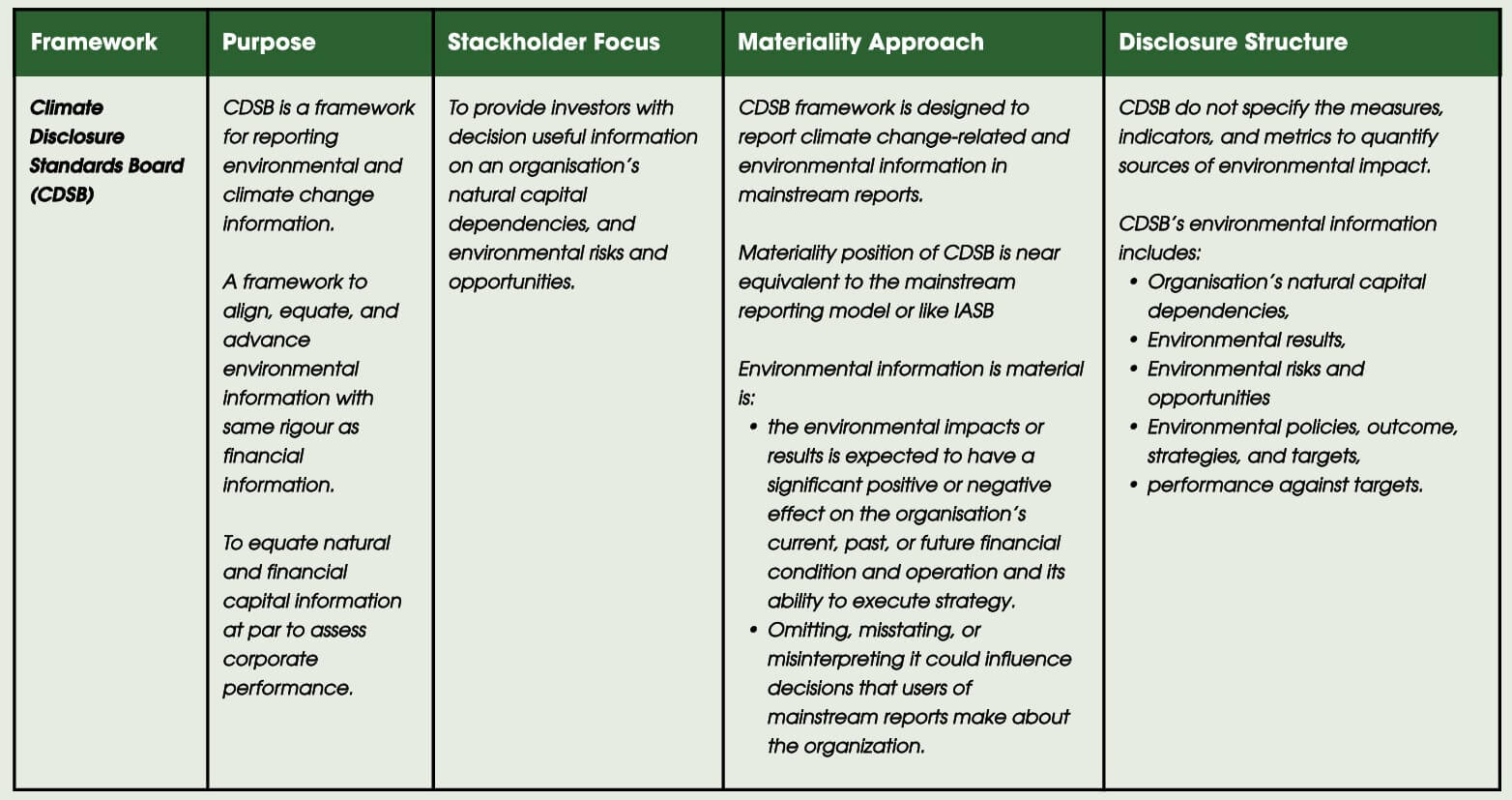

∅ Climate Disclosure Standards Board (CDSB).

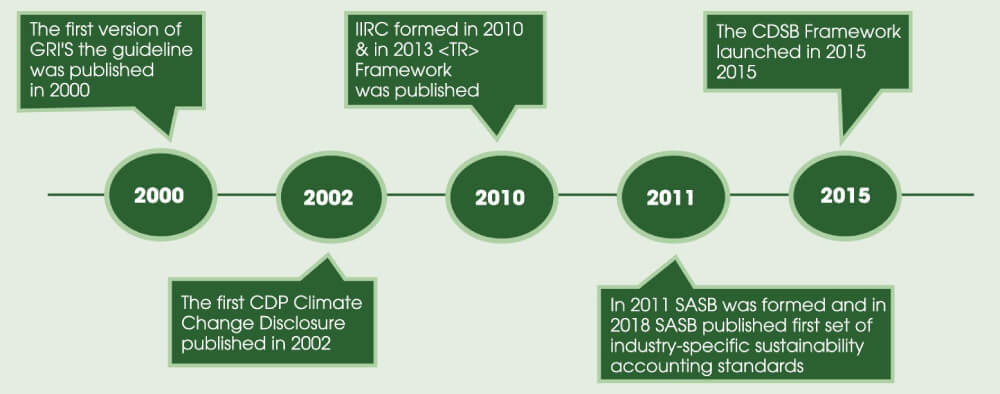

Figure 1: Timeline of Contemporary ESG Framework

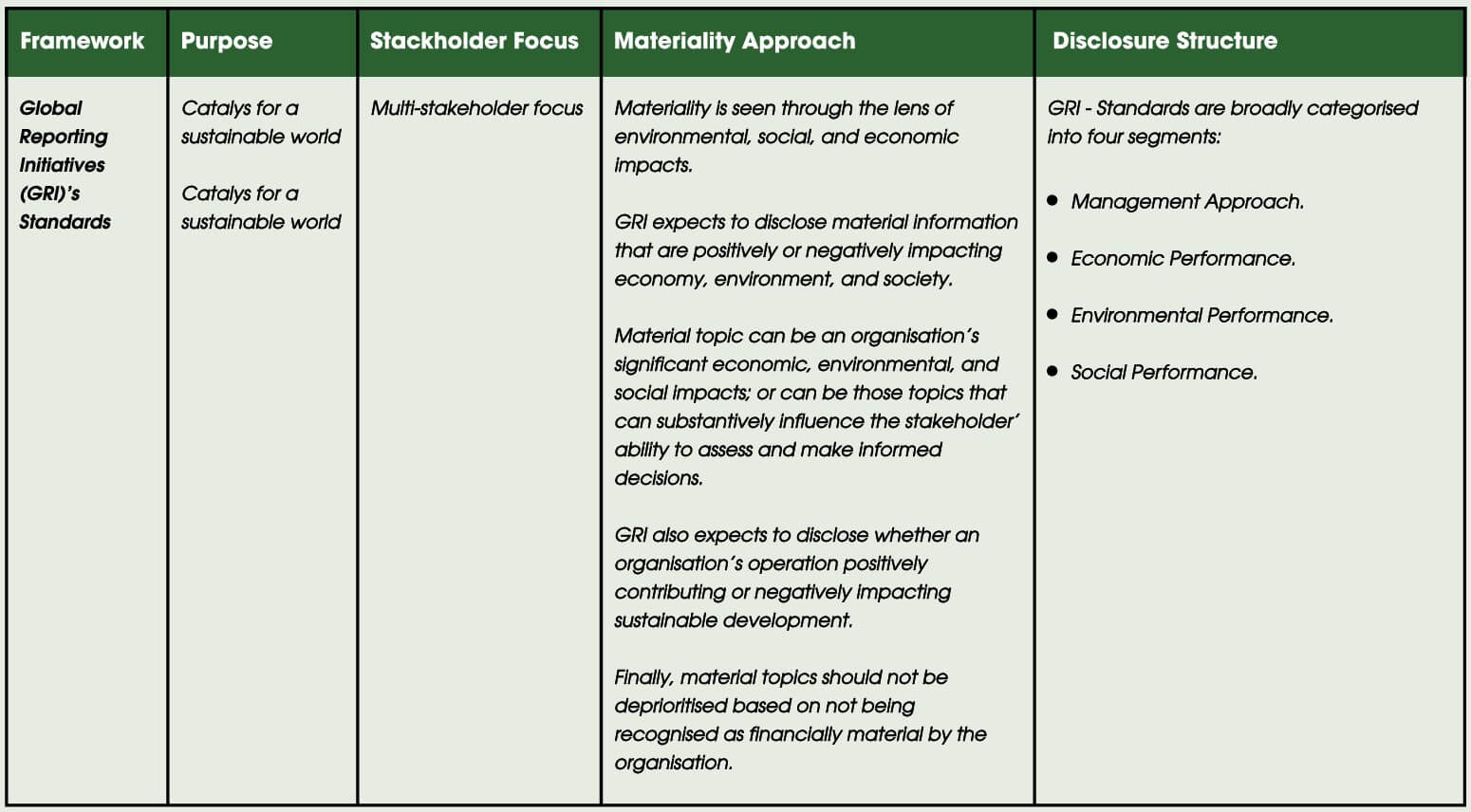

Global Reporting Initiatives (GRI.)

GRI provides multi-stakeholder-focused standards, and it has positioned itself as a catalyst for a sustainable world. The purpose of the standard is to support an organization’s and its stakeholders’ decision-making process about the organization’s economic, environmental, and social performance.

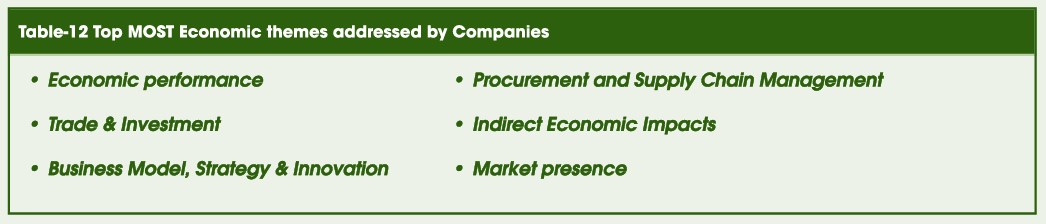

GRI’s sustainability topics include market presence, indirect economic impact, procurement practices, anti-corruption, anti-competitive behaviour, tax, material, energy, water, effluents, biodiversity, emission, waste, environmental assessment, employment, labour relation, OHS, training, diversity, equal opportunity, non-discrimination, freedom of association, child labour, forced labour, security practices, rights of indigenous people, human rights, local communities, supplier social assessment, public policy, customer health & safety, marketing & labelling, customer privacy, and socioeconomic compliance.

Table 2 An Overview of GRI Standards

GRI standards facilitate an organization to identify and report financial material positive or negative economic, environmental, mental, and social impacts of their operation on both the short- and long-term time horizons. As per GRI standards, an organization needs to identify material sustainability topics from two perspectives:

a) to identify those material sustainability topic areas of an organization’s operations that are positively or negatively impacted, as well as advancing or detrimental to sustainable development.

b) to disclose that information has the potential to influence stakeholders’ decision-making abilities and assessments significantly or substantively.

Most importantly, GRI strongly advocates that material sustainability topics should not be deprioritized based on not being recognized as financially material by the organization.

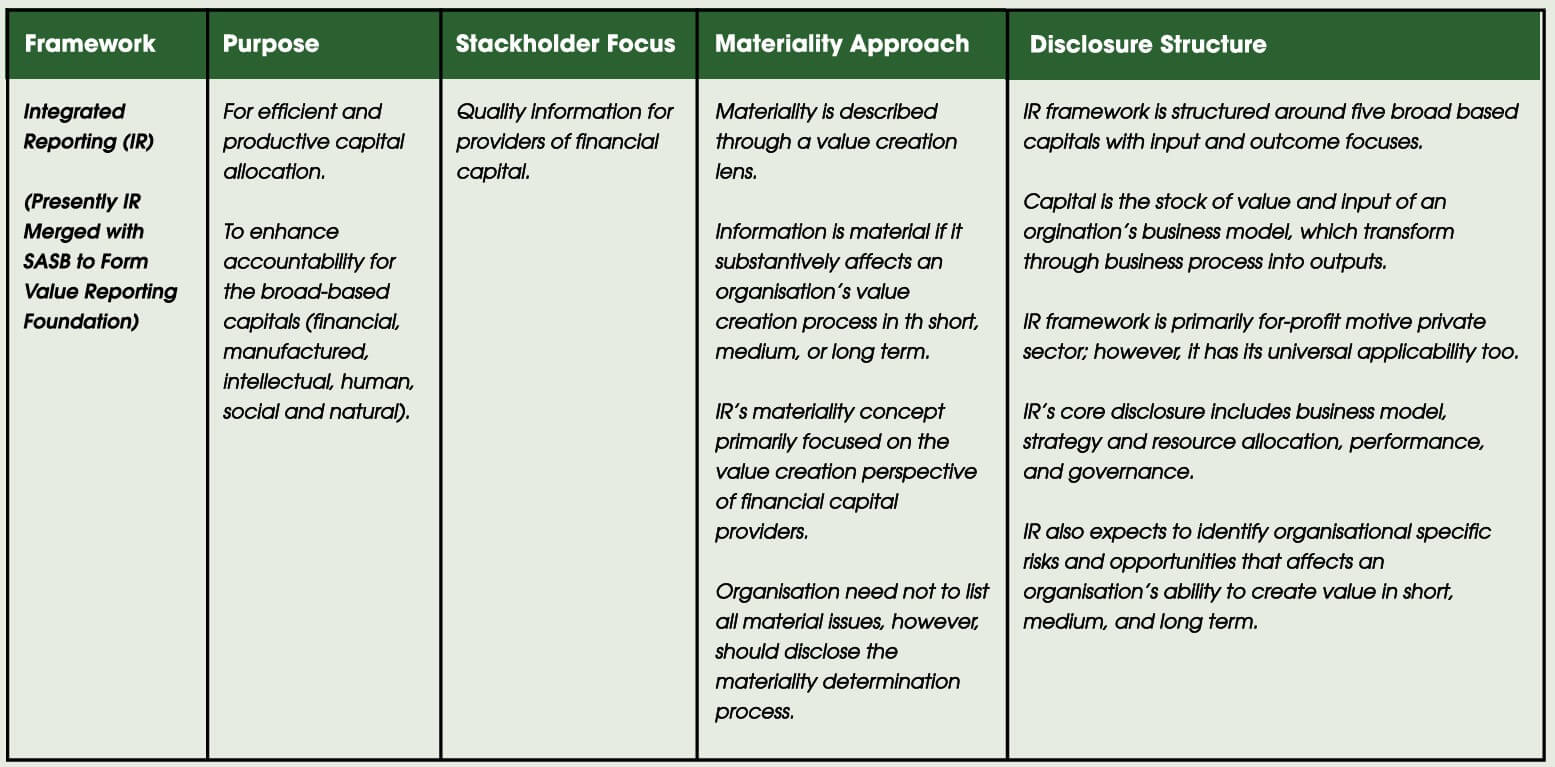

Integrated Reporting (IR)

The Prince’s Accounting for Sustainability Project (A4S) and the Global Reporting Initiative (GRI) formed the International Integrated Reporting Committee (IIRC) in 2010. Later, the committee was renamed The International Integrated Reporting Council (IIRC).

Integrated reporting is a principles-based framework founded on the concept of integrated thinking, which is a subset of systems thinking. The integrated reporting system informs financial capital providers about how businesses create value by efficiently utilizing five broad-based capitals (financial, manufactured, intellectual, human, social, and natural). Capital is the stock of value and input of an origination’s business model, which transforms through business activities into outputs. Hence, an Integrated Report defines material information through the prism of value creation.

Table 3 An Overview of Integrated Report

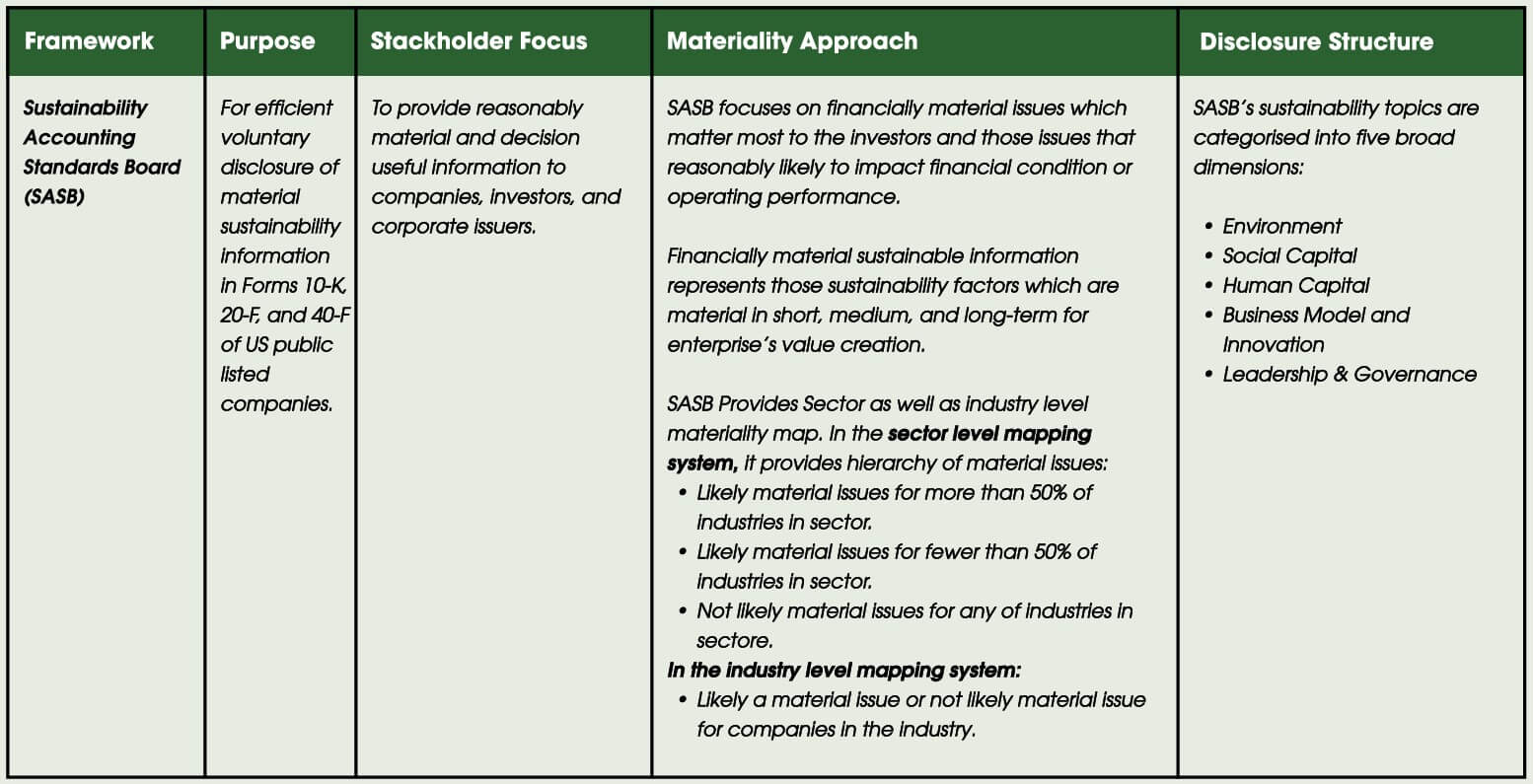

Sustainability Accounting Standard Board (SASB)

SASB was established in 2011 as a not-for-profit organization to develop sustainability accounting standards for investors, lenders, and businesses in the USA. SASB provides sector-specific metric-based voluntary reporting standards. It encompasses eleven sectors and seventy-seven industries.

∅ Consumer goods (7 industries),

∅ Extractive and minerals Processing (8 industries),

∅ Financials (7 industries),

∅ Food and beverages (8 industries),

∅ Health Care (6 industries),

∅ Infrastructure (8 industries),

∅ Renewable Resources & Alternative Energy (6 industries),

∅ Resource Transformation (5 industries),

∅ Services (7 industries),

∅ Technology & Communications (6 industries),

∅ Transportation (9 industries).

SASB covers five broad topics: environment, social capital, human capital, business model and innovation, and leadership and governance.

SASB’s sector-specific sustainability topics include:

In the context of SASB, sustainability information is material if it is financially material and can impact an enterprise’s value-creation process in the short, medium, and long term. SASB also prescribes a sector and an industry-level materiality mapping tool. The materiality map helps corporations to strategize sustainability goals and provides the metrics to underpin disclosure topics. For an investor, the materiality map provides a tool to analyse an industry or sector issue alongside specific sustainability risks and opportunities.